Key Takeaways

- Blockchain is a digital database that records and stores data across a network of computers.

- Blockchain can support various applications, including cryptocurrencies, smart contracts, and supply chain tracking.

Whether you’re a cryptocurrency veteran or don’t know much about coins, you might want to understand blockchain. While many associate this digital technology with cryptocurrencies like bitcoin, blockchain’s potential could extend beyond just digital currencies, possibly reshaping entire industries.

What is Blockchain?

At its core, blockchain is an online database, much like a spreadsheet you might use for work or at home. However, this database (or “ledger,” in blockchain terminology) is decentralized and distributed: Instead of the data being stored in one location on a single computer or server, a network of unrelated computers, called “nodes,” each maintain their own copy of the ledger. The decentralized nature of the ledger ensures the reliability of the data, as someone would have to corrupt multiple copies to deceive the network.

How Does Blockchain Work?

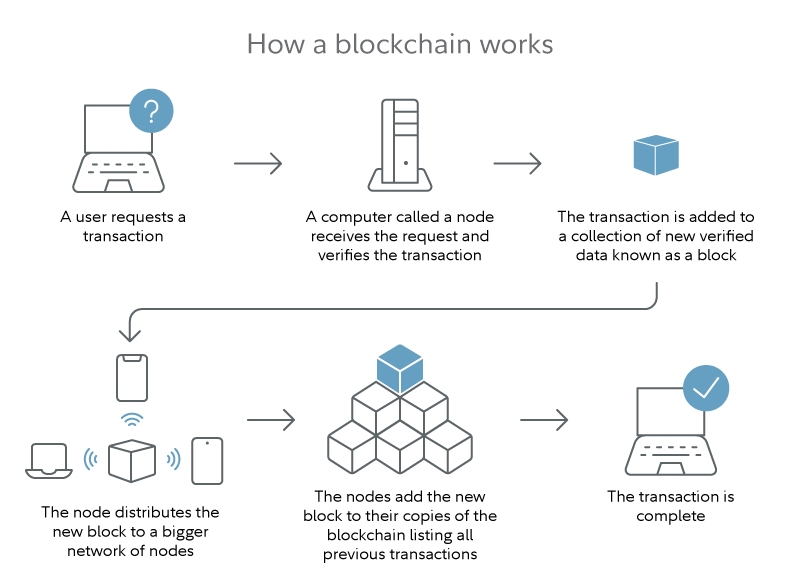

To understand how blockchain works, let’s break down its name: A “block” is a unit of data storage, such as transaction data. Blocks generally contain multiple data points (e.g., more than one transaction). Once a block reaches its storage capacity, it is added to the chain of blocks that came before it.

Blocks are designed to be unchangeable once added to the chain. This ensures that anyone using blockchain software can trace the history of data from the blockchain’s inception to the present.

Not just anyone can add data to a blockchain. This ability is restricted to individuals and organizations running blockchain software on computer nodes. Typically, they update the blockchain by using computing and electricity resources to solve complex mathematical problems (a process called “proof of work”) or by staking a small amount of cryptocurrency that they will lose if they approve fraudulent transactions (a process known as “proof of stake”). These are called “consensus mechanisms,” processes through which blockchain participants agree on the validity of transactions.

Once a node approves a transaction, that information is distributed to all other nodes, so they can update their copies of the blockchain ledger collectively.

In theory, blockchain systems are secure because a hacker would need to control more computing power than the majority of the network (a challenging task), risk losing their crypto holdings if they approve fake transactions, or control at least 51% of the nodes to force all nodes to accept fake data.

While it’s unlikely for a well-established blockchain with many nodes to be hacked, newer systems with fewer nodes may be more vulnerable. Nevertheless, blockchain’s infrastructure makes it far more difficult—and potentially costly—to hack.

How is Blockchain Used?

Blockchain provides a framework for new technologies, whether it’s cryptocurrencies or record-keeping platforms that could revolutionize industries such as supply chain management or online identity verification.

Cryptocurrencies are the most well-known application of blockchain technology. In fact, most major cryptocurrencies, including bitcoin and Ethereum, operate on blockchain systems.

Crypto blockchain ledgers record transactions made with a specific cryptocurrency and provide mechanisms to prevent fraudulent activities like double spending (where someone attempts to spend the same cryptocurrency multiple times). Since the blockchain is constantly updated and shared with other nodes, it is difficult to trick a node into allowing a coin to be spent again once it has left the user’s possession.

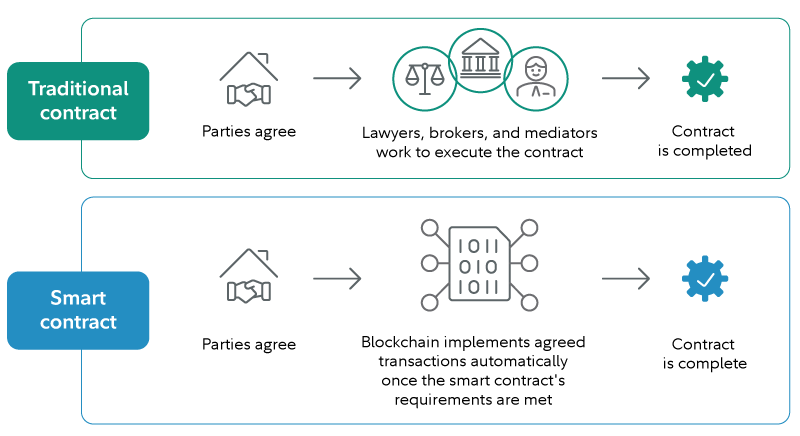

A smart contract is a computer program that uses blockchain to automatically execute agreements or contracts. It earns the “smart” label because it can automatically trigger transactions when certain conditions are met and recorded in a block.

In the past, a middleman—such as a lawyer, broker, or mediator—would be needed to ensure that such transactions took place. Now, instead of paying for escrow services or hiring an attorney, a smart contract can ensure funds are transferred after an agreed-upon condition is fulfilled. The self-executing nature of smart contracts could reduce costly processing fees, benefiting multiple industries.

However, smart contracts are not a perfect replacement for traditional contracts. Depending on how they’re written, they can be difficult to modify once set and are susceptible to hacks or bugs.

Blockchain can also be used to track and verify ownership of items, such as real estate or art. It has gained popularity with “non-fungible tokens” (NFTs), unique digital assets built using blockchain, usually on the Ethereum network. NFTs allow users to instantly verify an asset’s authenticity and trace its ownership history.

Unlike digital files, which can be copied endlessly, NFTs cannot be reproduced. This scarcity can increase their value, assuming demand remains. Furthermore, thanks to smart contracts, NFTs can pay royalties to creators from future sales—something that doesn’t usually happen with secondary sales of traditional artwork.

Manufacturers can also use blockchain to track their products along the supply chain. For example, in the food industry, blockchain technology allows stakeholders (farmers, distributors, producers, and vendors) to ensure transparency from farm to grocery store. Consumers can see the full history of a food product, which helps verify claims such as “organic” or “fair trade.”

Advantages of Blockchain

Decentralization

Because blockchain ledgers are decentralized and distributed across many nodes in different locations, they are harder to tamper with compared to centralized records. It would be easier for a hacker to alter financial data in a centralized database (like a bank’s) than to manipulate a distributed blockchain’s nodes.

However, simply distributing data across multiple locations doesn’t equate to decentralization. A system is truly decentralized when all participants have equal rights to update the transaction log and there are no centralized authorities. This ensures that blockchain systems continue to function even after the organizations that created them have disappeared.

Increased Transparency

Blockchain systems inherently provide transparency to users with access to the network, enabling them to inspect the transaction ledger and monitor for fraud or manipulation.

Although cryptocurrencies are often associated with anonymity, there is a public record of every movement made with its native digital coin on the blockchain. In some cases, this transparency can help authorities track money laundering activities if they can link a public crypto wallet address to illicit activity.

Disadvantages of Blockchain

Energy Consumption Concerns

Some blockchain systems require significant energy, which can be harmful to the environment if powered by unsustainable sources. In 2021, the energy needed to run the Bitcoin network accounted for 0.55% of the world’s electricity consumption, though 38% to 73% of this energy came from renewable sources like wind and hydroelectric power.

As blockchain technology continues to grow, it will be crucial for individuals, companies, and governments to assess whether the benefits outweigh the environmental costs.

Changing Regulations

As blockchain and cryptocurrencies are relatively new technologies, governments are still figuring out how to regulate them. In the U.S., for example, access to crypto exchanges and specific cryptocurrencies may differ by state.

On a larger scale, the regulatory uncertainty presents risks for blockchain technology and cryptocurrency investors. Governments may outlaw certain blockchain applications or impose taxes that hinder long-term growth. Additionally, the volatility of crypto assets makes them more susceptible to market manipulation, and they do not benefit from the same regulatory protections as registered securities. Crypto is also not insured by the FDIC or SIPC, so investors should only buy crypto with money they can afford to lose.